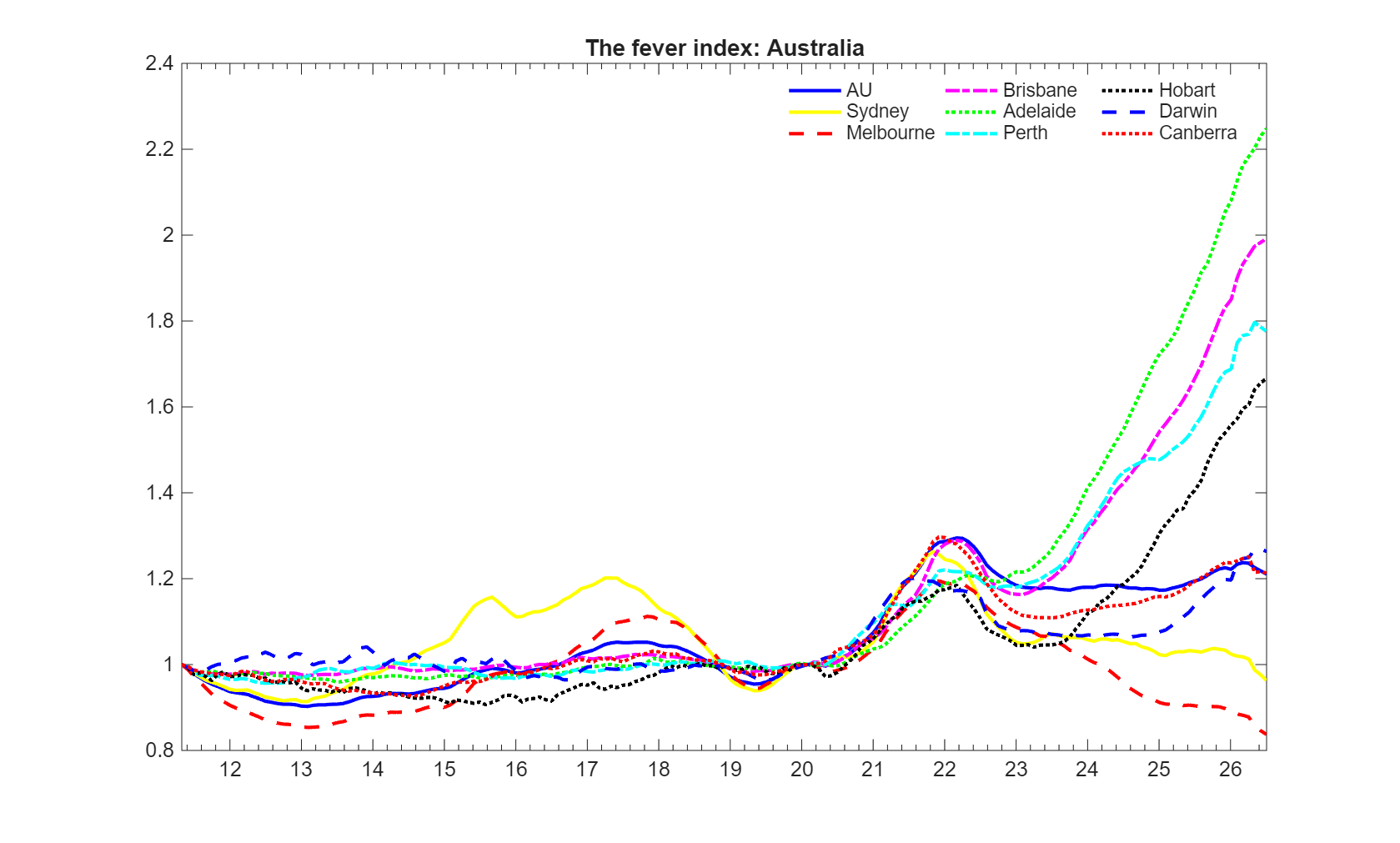

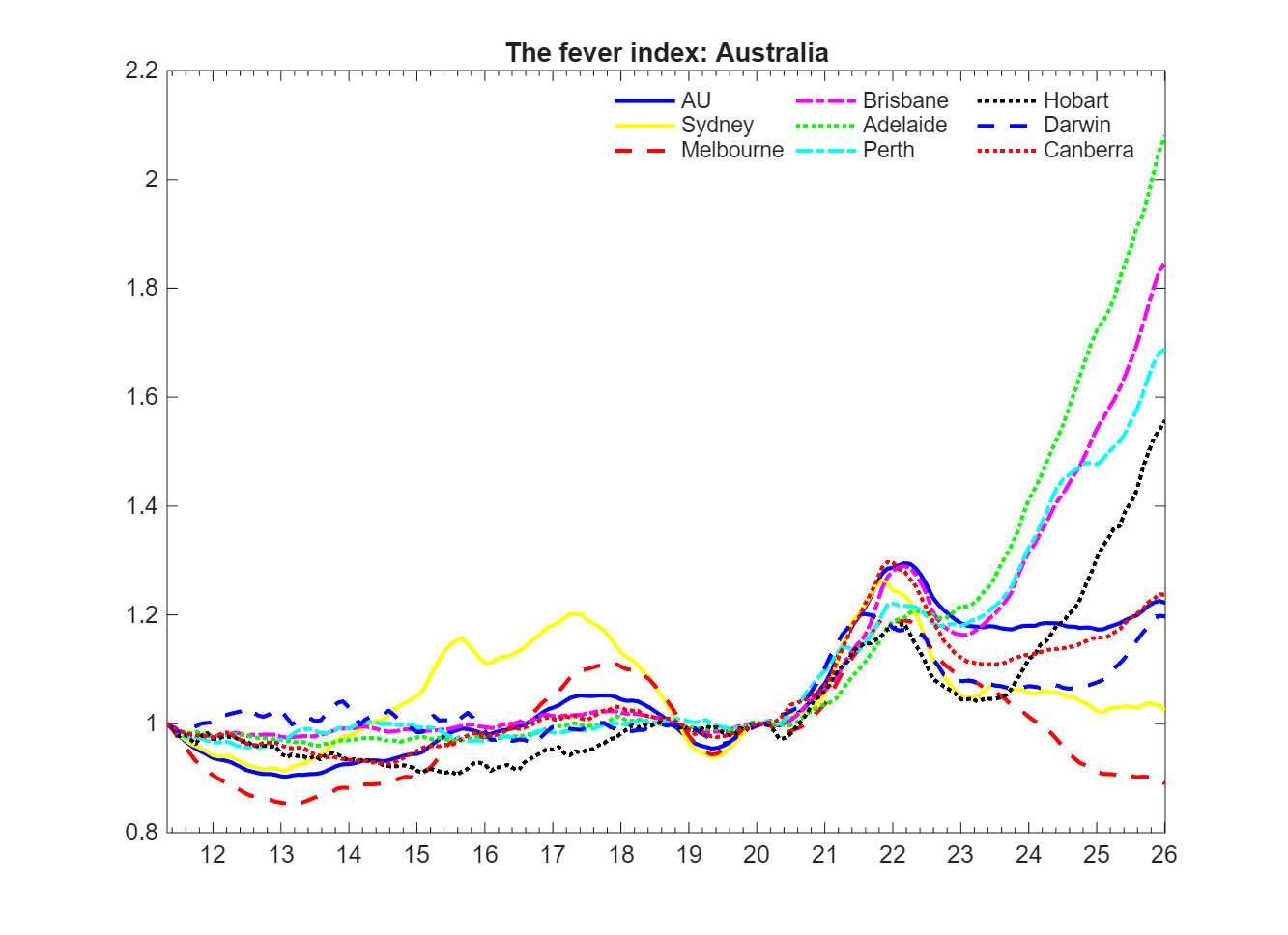

This website provides real-time bubble indicators for housing markets in the eight Australian capital cities and primary New Zealand regions. These indicators provide a direct quantitative measure of the extent of housing fever in these major metropolitan areas. The measures are benchmarked against housing and macroeconomic fundamentals so that they provide a statistical mechanism for assessing the existence and the degree of speculative behaviour in these housing markets.

The markets considered are as follows.

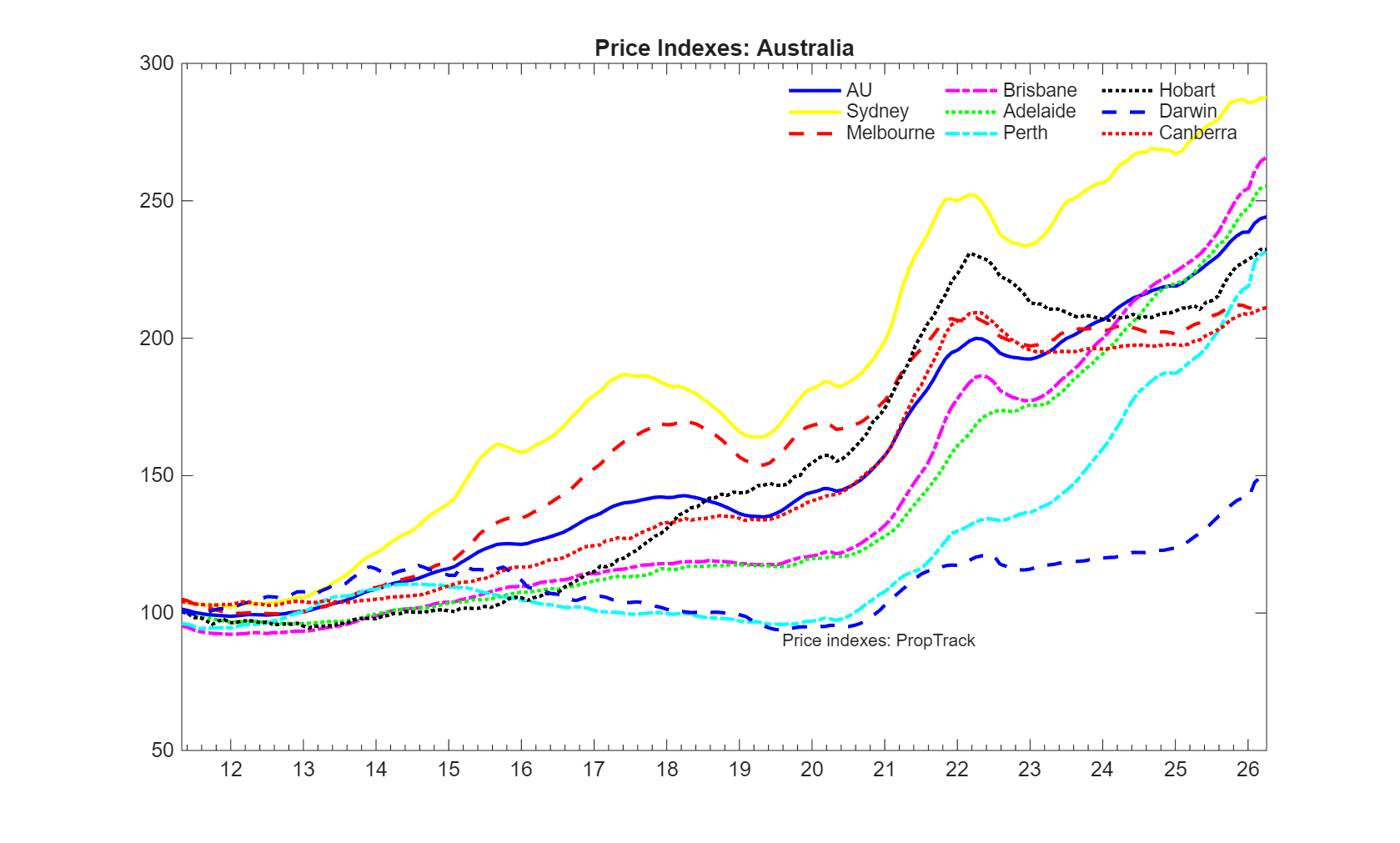

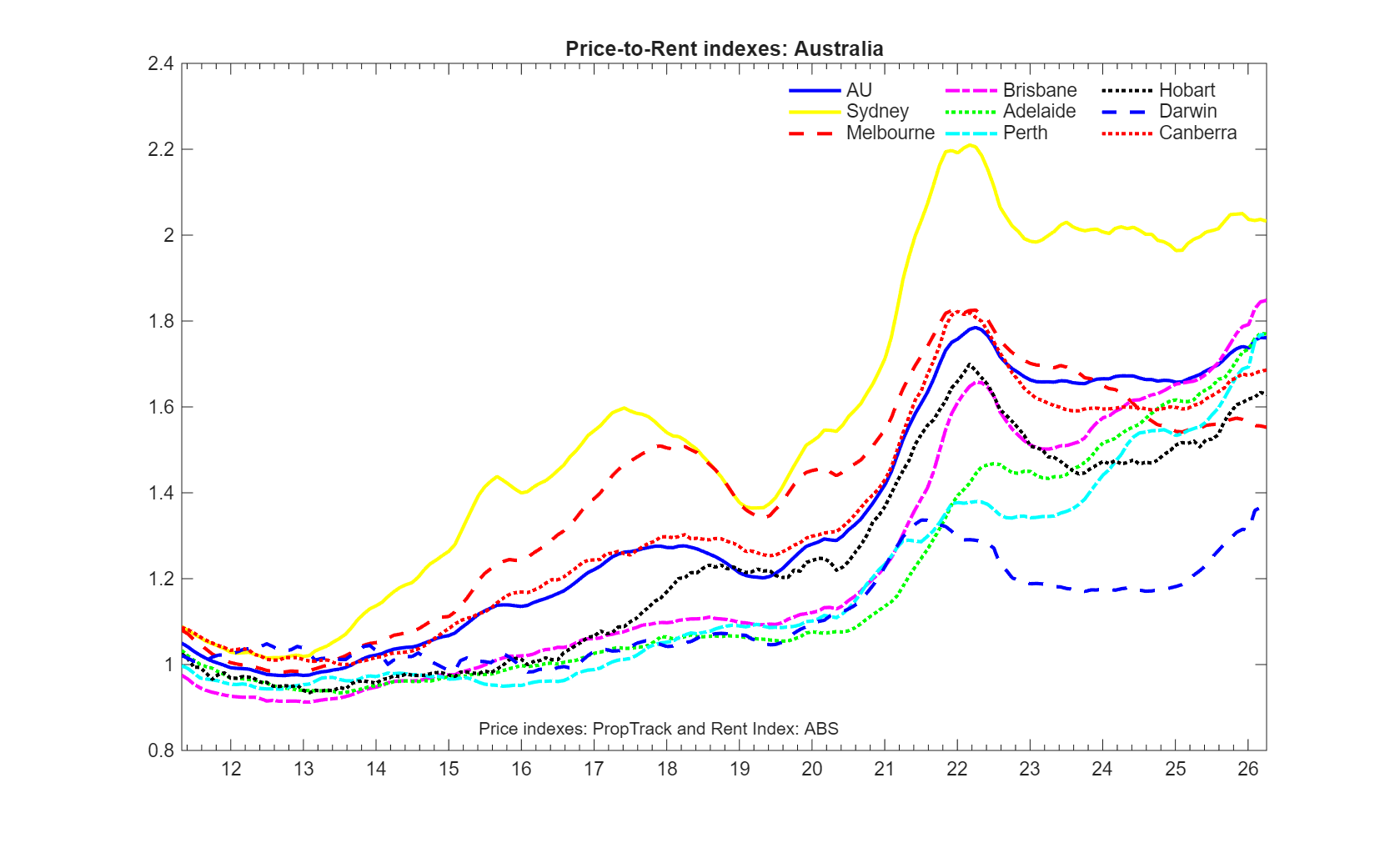

- Australia: Sydney, Melbourne, Brisbane, Adelaide, Perth, Hobart, Darwin, and Canberra

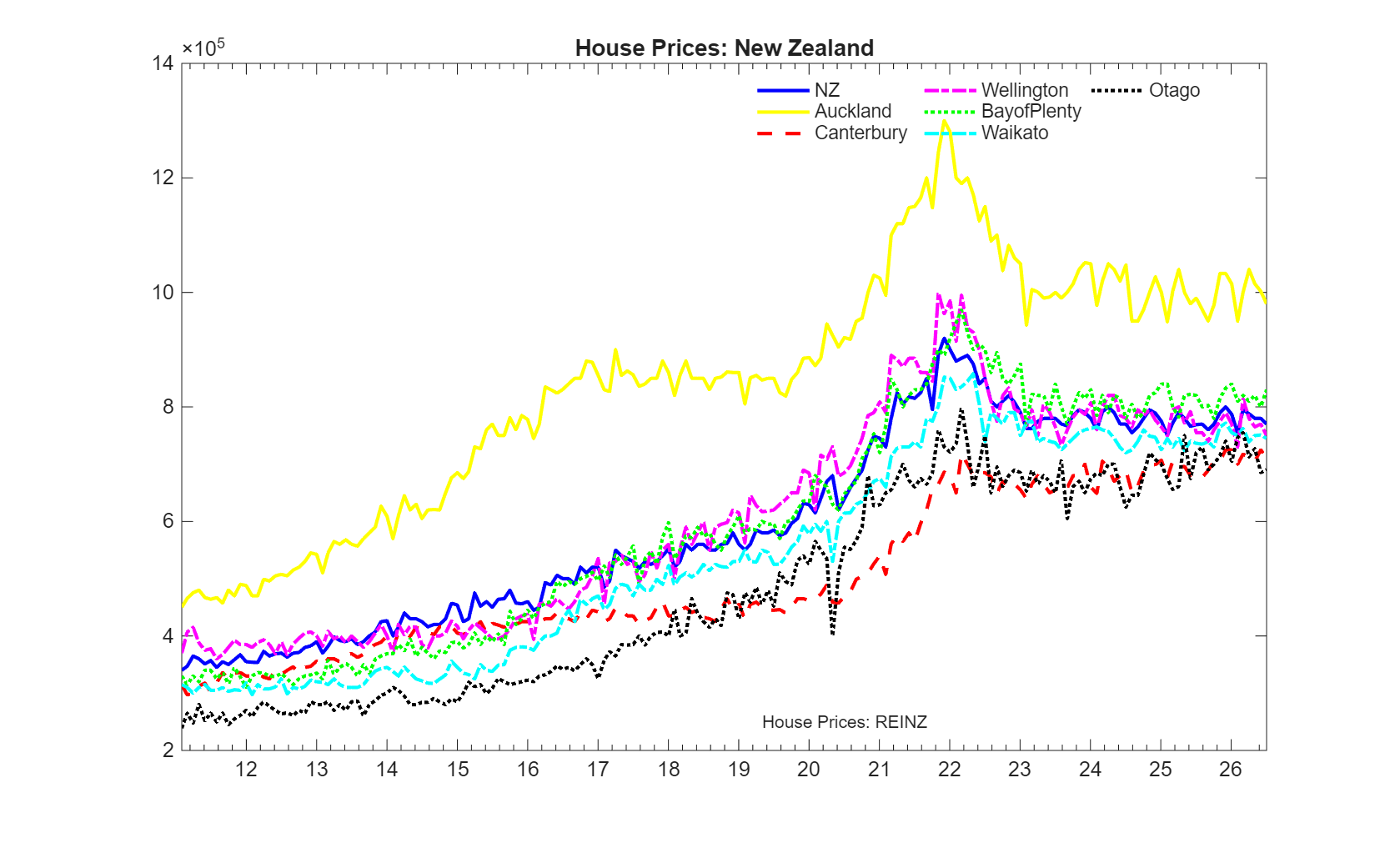

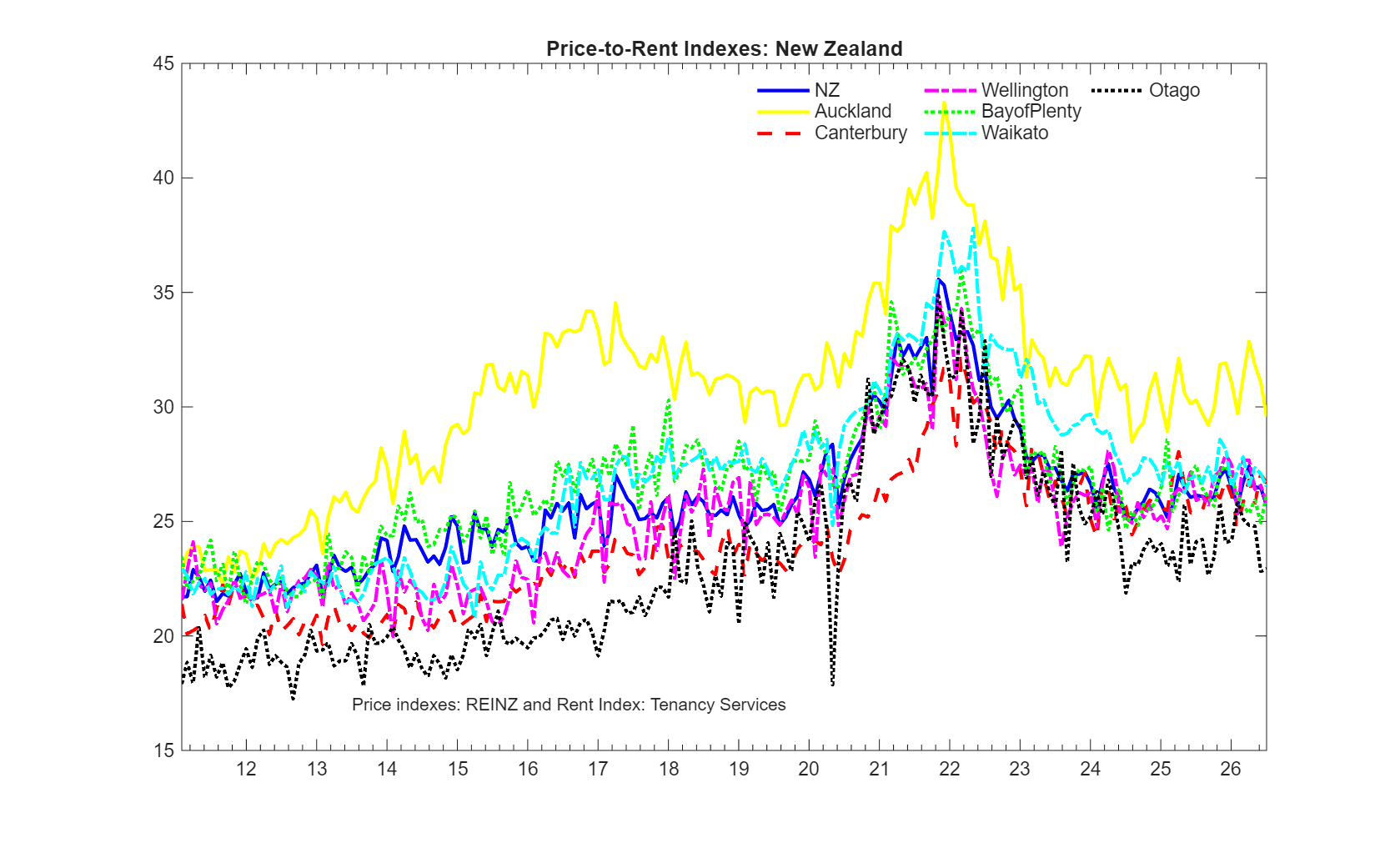

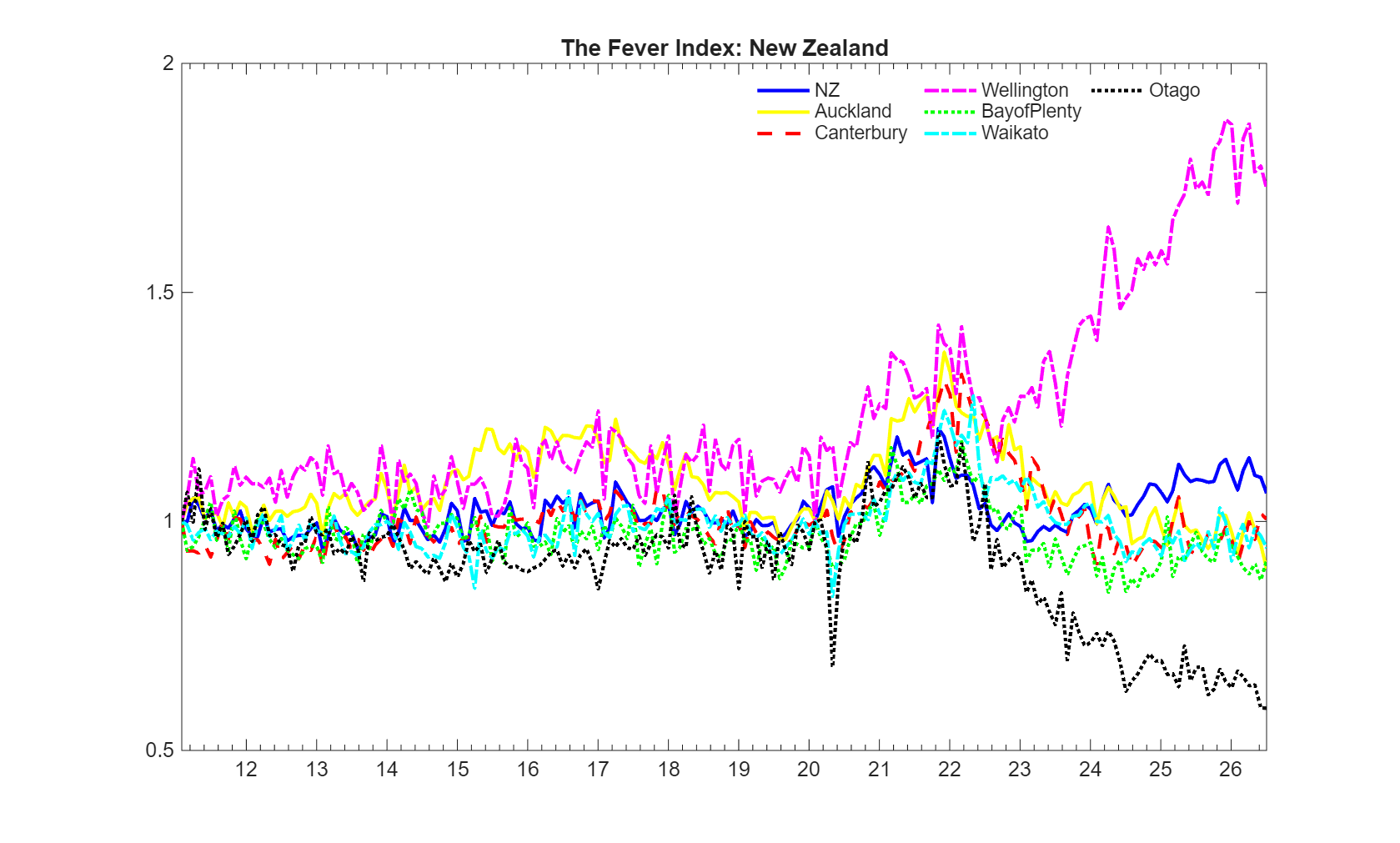

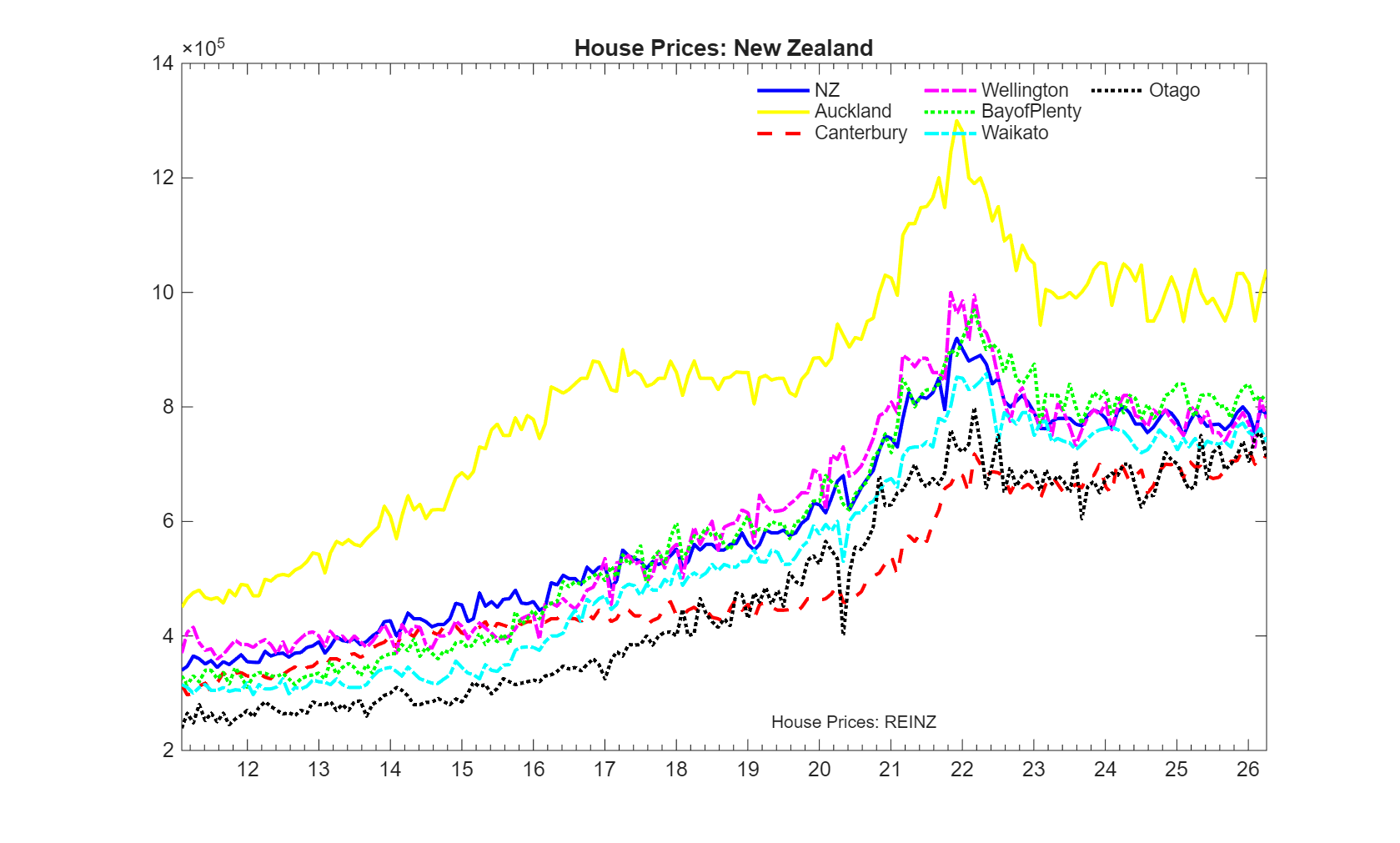

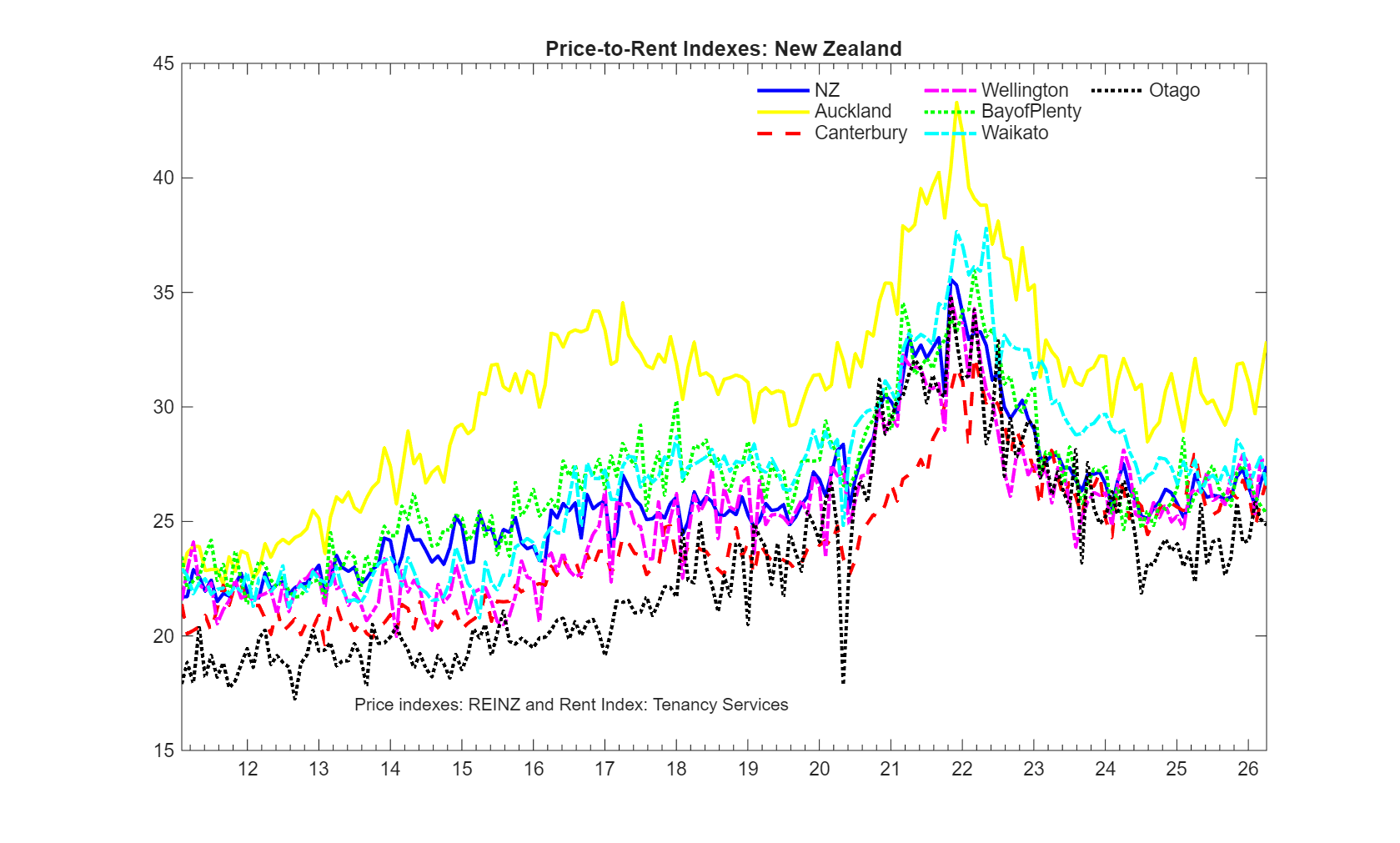

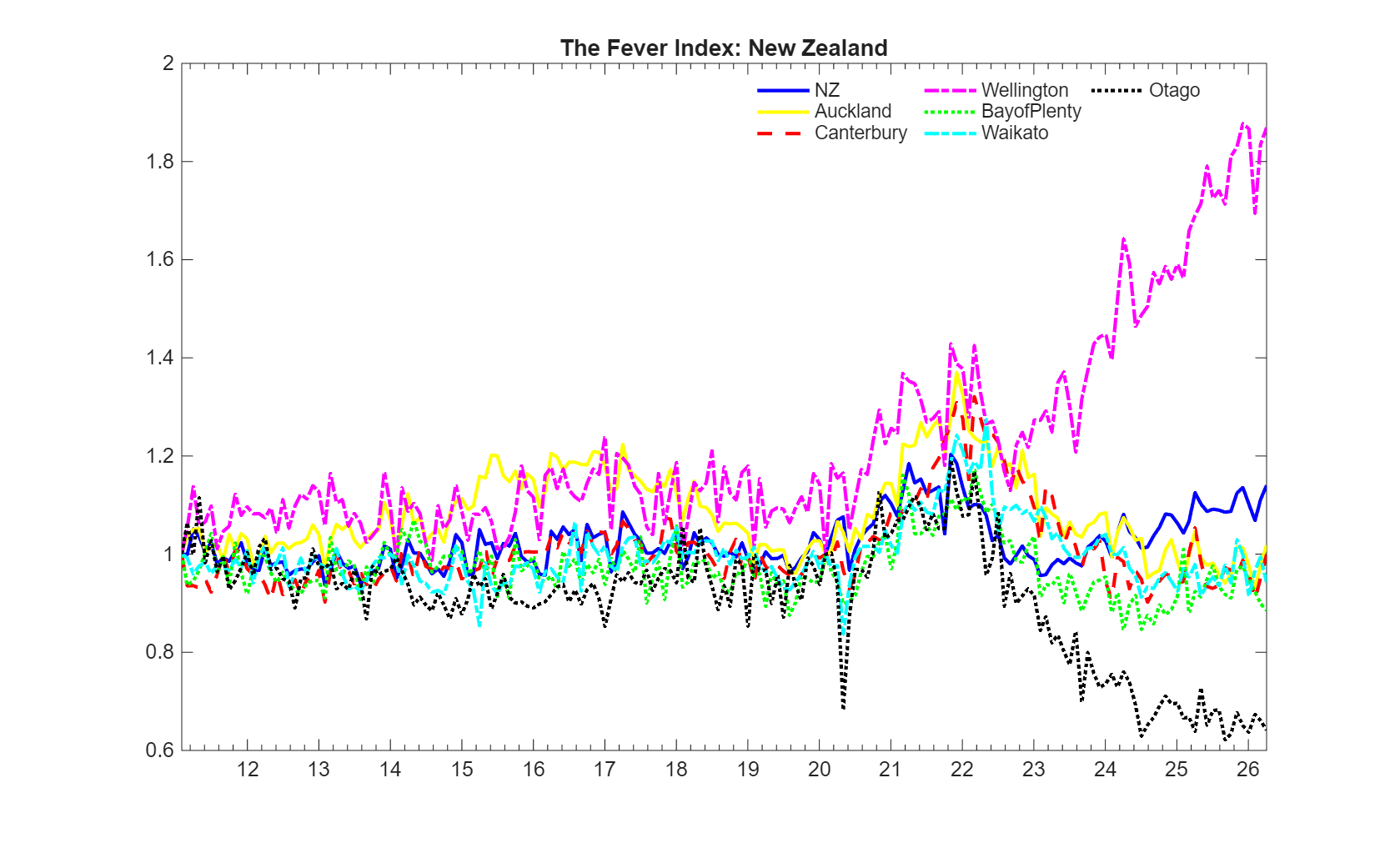

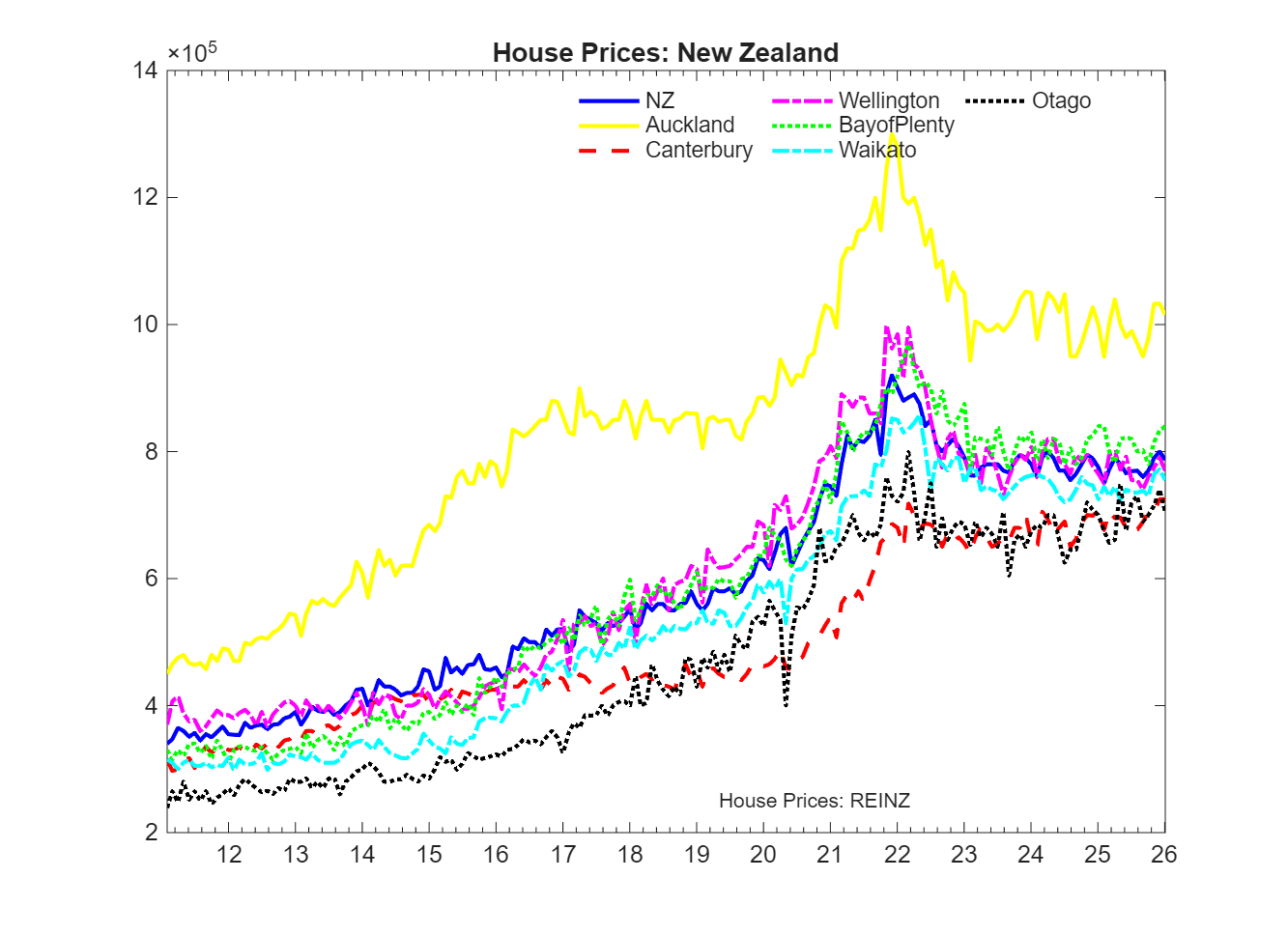

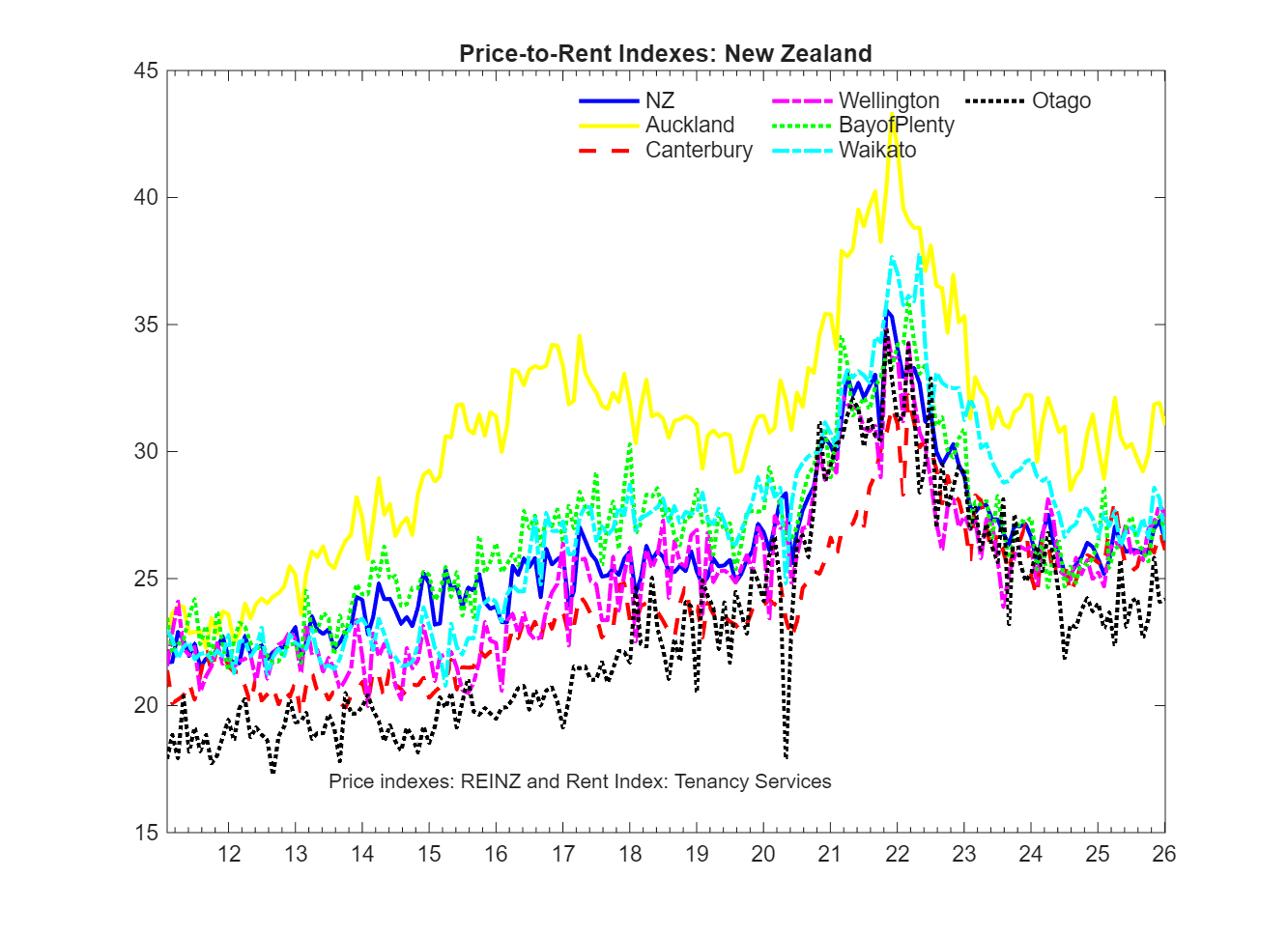

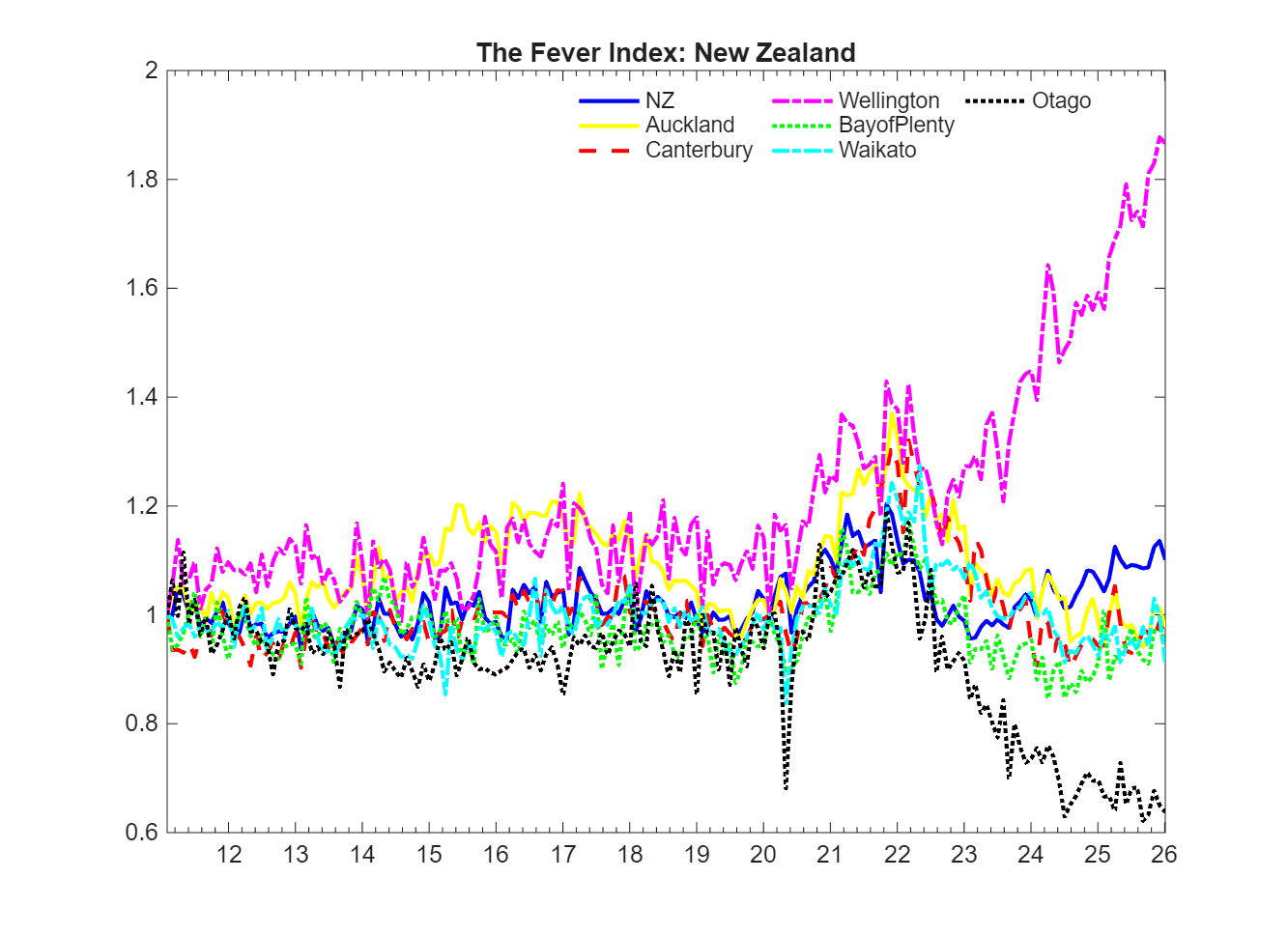

- New Zealand: Auckland, Canterbury, Wellington, Bay of Plenty, Waikato, and Otago

June 2026

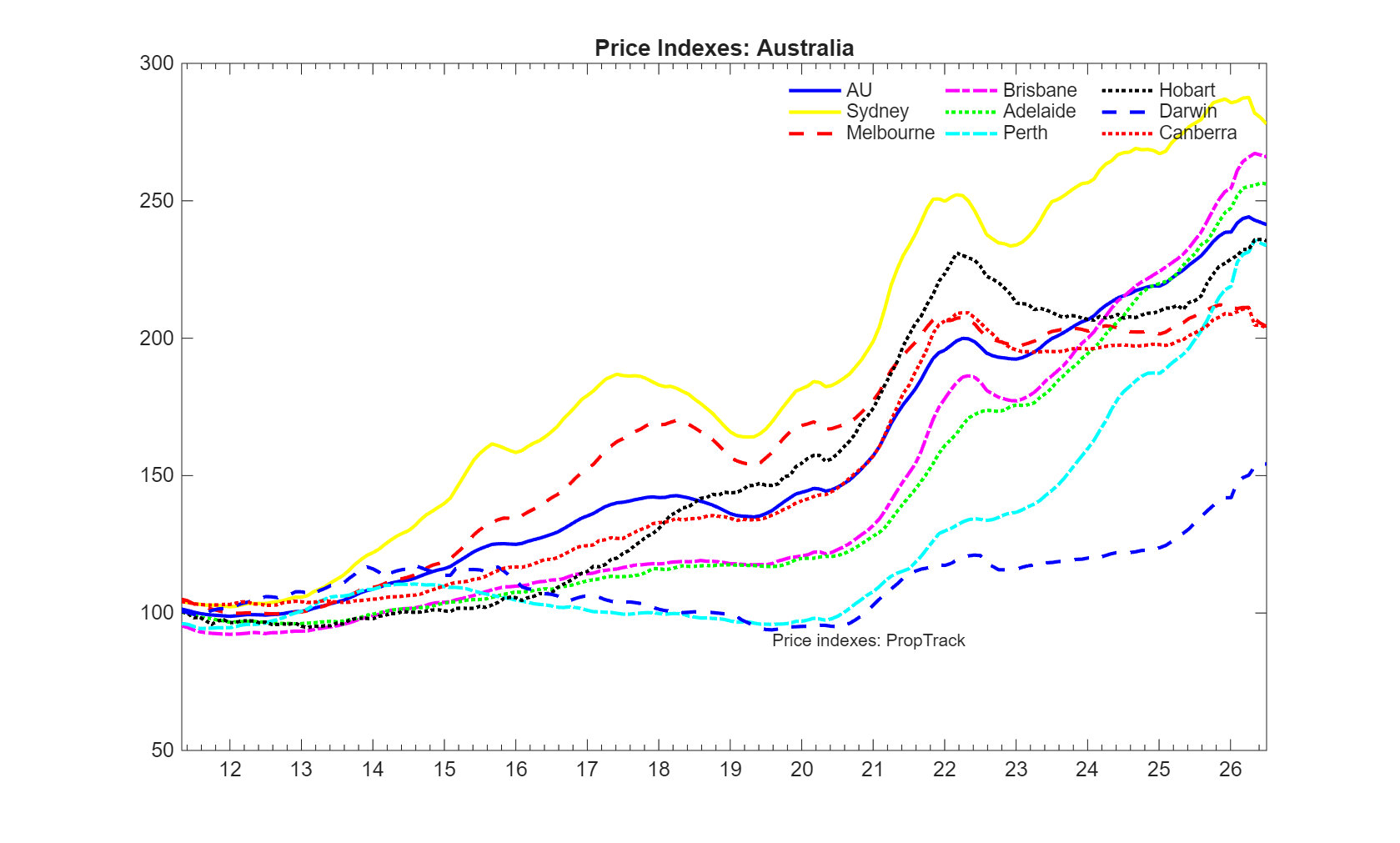

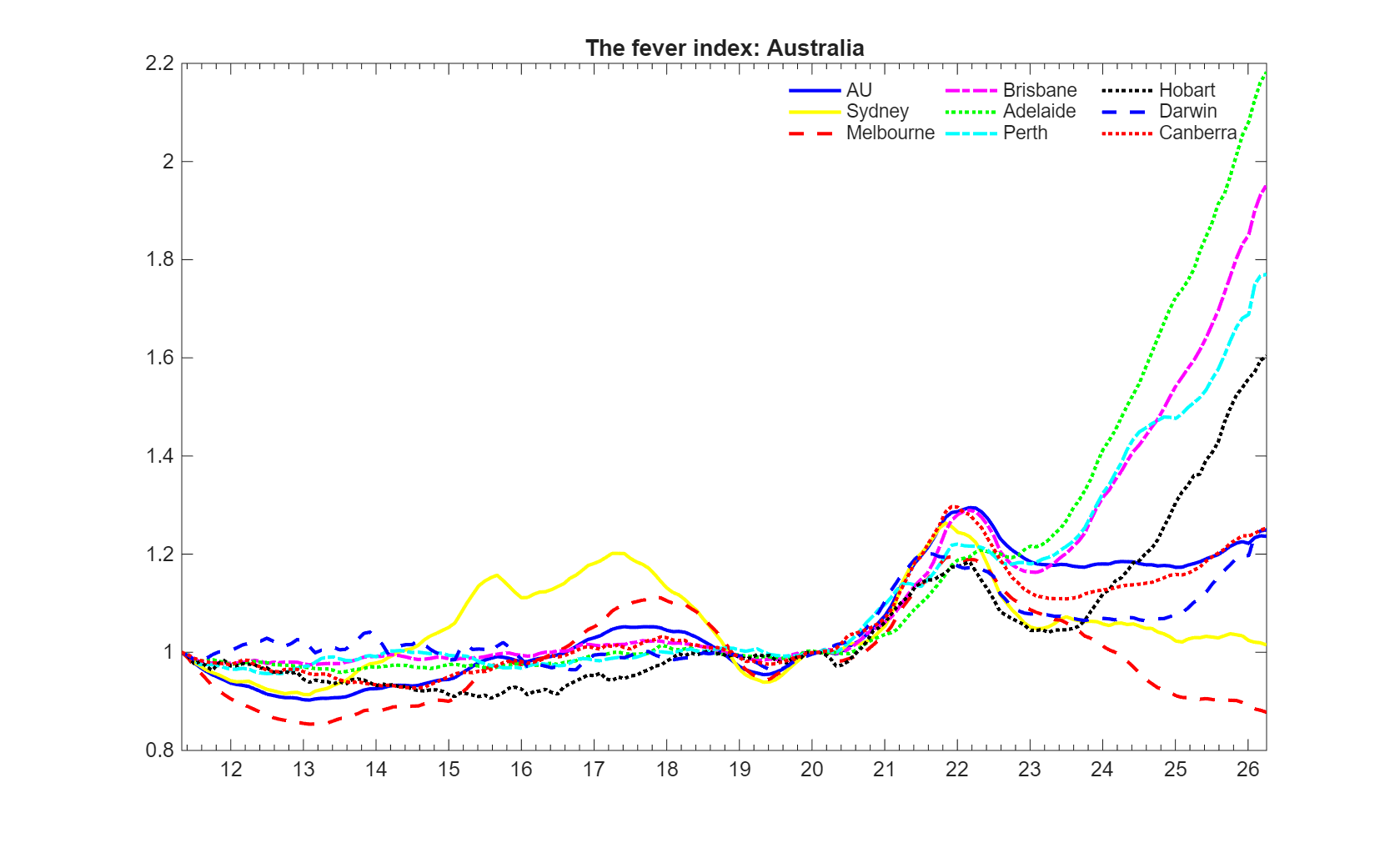

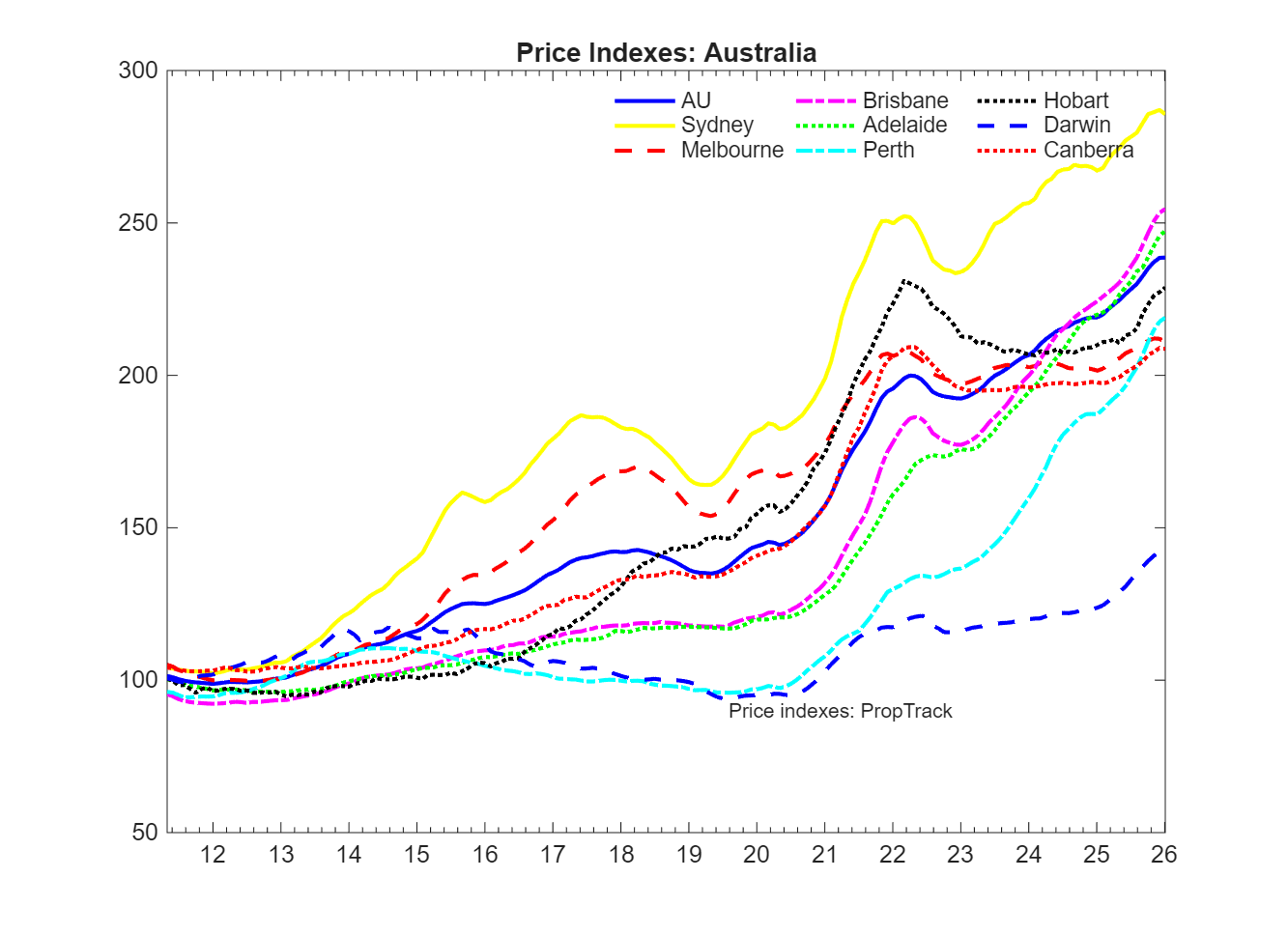

Australia The Australian housing market cooled over the June quarter of 2026, with the divergence observed in recent quarters beginning to narrow. Prices fell in Canberra, Sydney, and Melbourne, each by around 3 per cent over the quarter, while Brisbane and Adelaide were essentially flat. Perth, Hobart, and Darwin continued to record gains, but at

March 2026

Australia March 2026 shows a growing divergence in Australian capital city housing markets. Brisbane, Adelaide, and Perth are leading a steep upswing in prices, with Darwin also showing a sharp acceleration in recent months. Hobart continues to experience steady growth. In contrast, Canberra and Sydney are plateauing, while Melbourne has begun to show slight price

December 2025

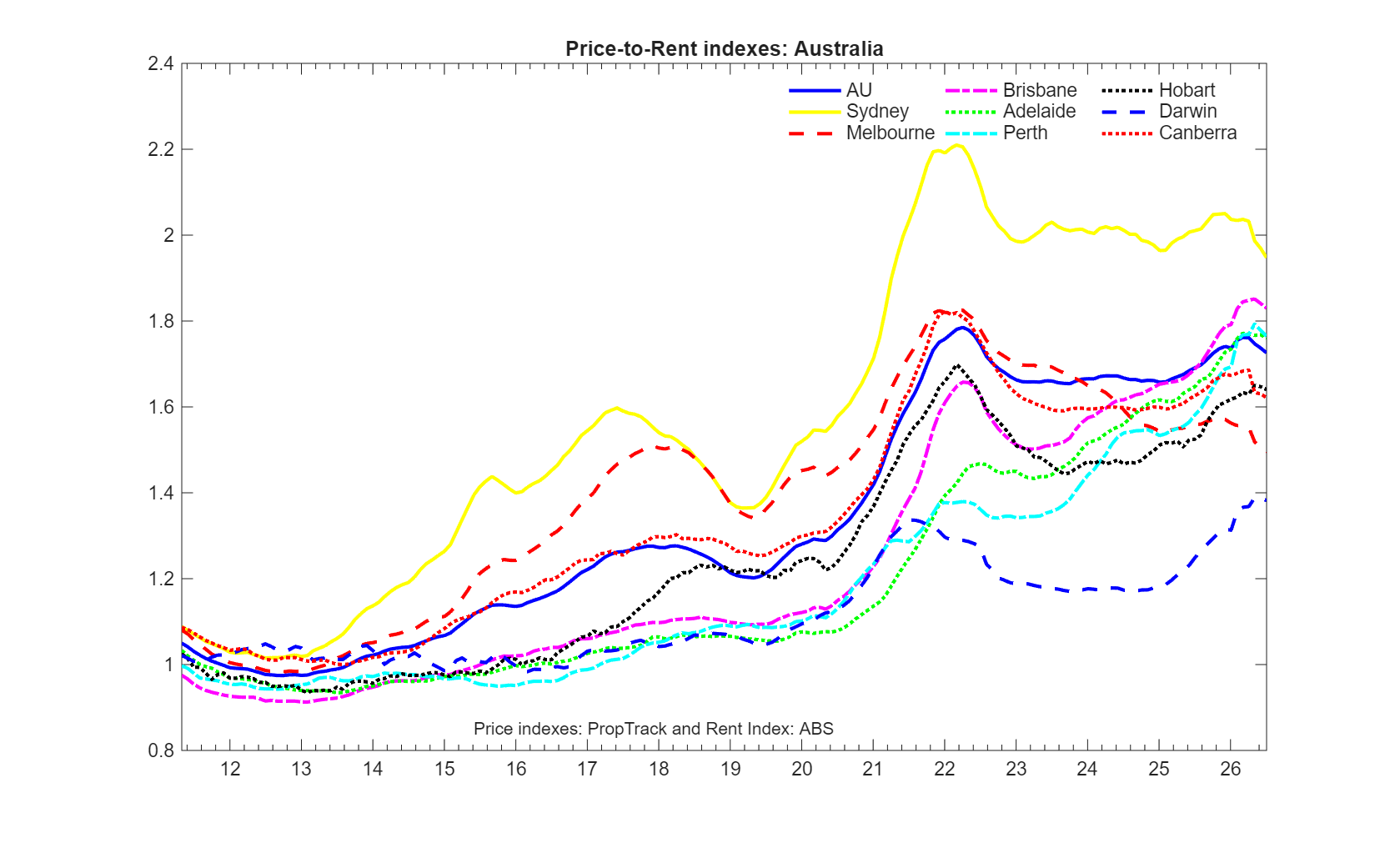

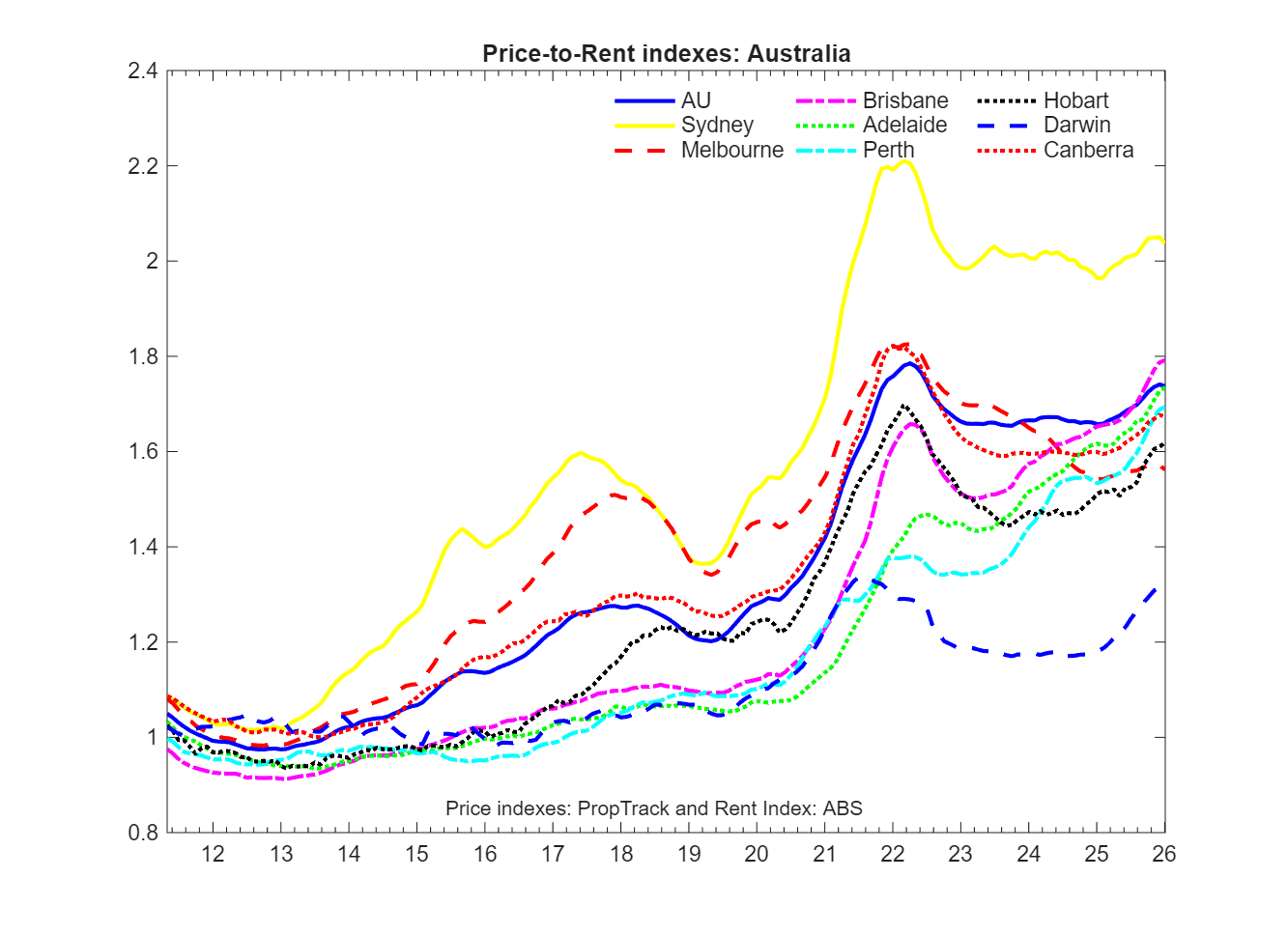

Australia December 2025 found housing prices rising across all Australian capitals but at markedly different speeds. Brisbane, Adelaide, Perth, and Hobart lead the upswing, while Canberra, Melbourne, and Darwin show more subdued growth. Price-to-rent ratios, which focus on the relationship between prices and rental fundamentals, point to renewed valuation pressure in Brisbane, Adelaide, Perth, Hobart,

This project is supported by the Australian Research Council under Project No. DP190102049.